Nov 13, 2020

Value Investing: What Does this Mean and How does it Impact You? (Part 1)

Written By: Spencer Kenley

In the world of investments, one way to classify stocks is to differentiate between what are known as “growth” and “value” stocks. The difference is this: growth stocks are relatively more expensive than value stocks; in other words, a growth stock means that an investor must spend more upfront to own the same amount of company assets.

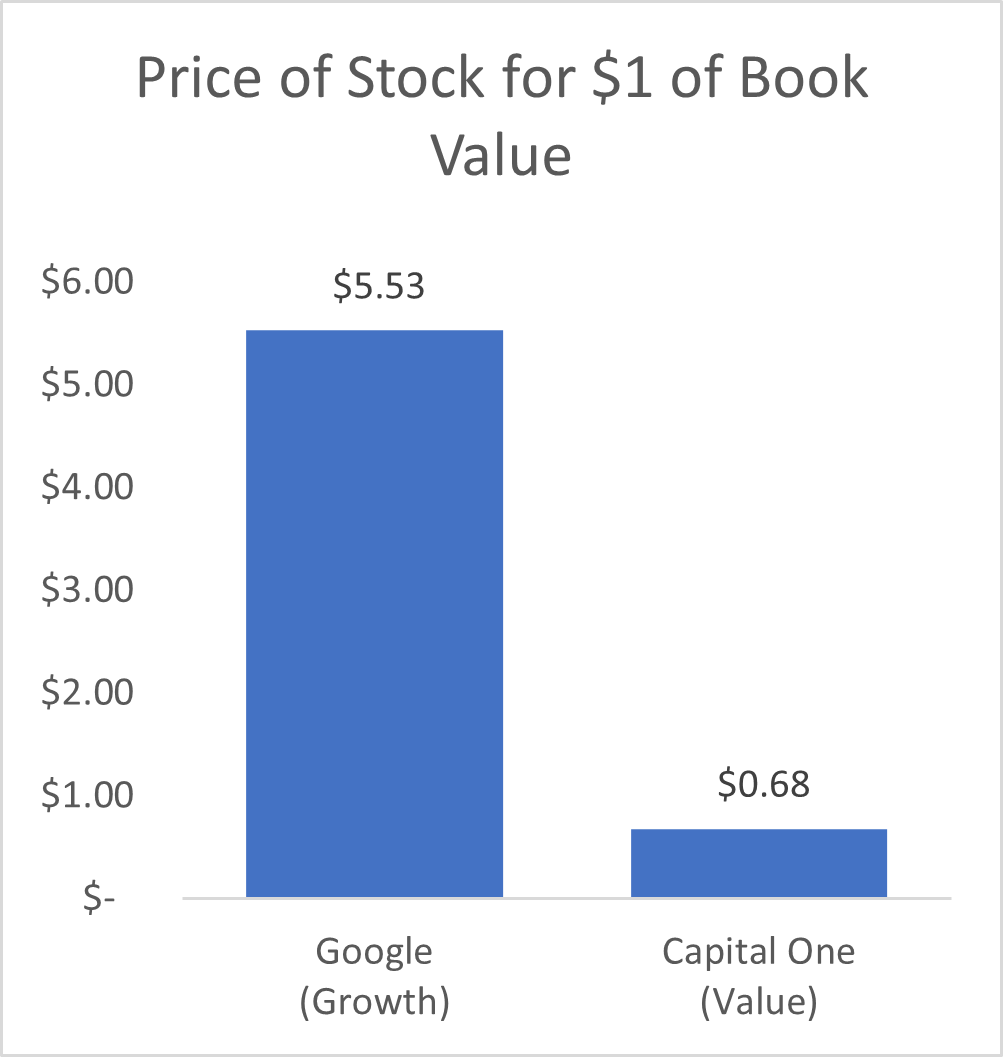

Let’s look at an example: right now, Google is a “growth” company; if you add up the price of all Google stocks in the world (about $1.19 trillion as of November 11, 2020 – a huge amount to say the least!), it will outweigh the value of the equity on Google’s balance sheet by about 5.5 times. On the other hand, Capital One Financial Corp’s $38.73 Billion of market value is only 68% of the value of book equity. Roughly speaking, that would mean that a $0.68 investment in Capital One would entitle the investor to $1 of assets on the balance sheet. On the other hand, an investor in Google would have to shell out about $5.53 for the same amount of equity in Google![1]

So how does this apply to your investments? Academic research has shown that, over the long-term, value stocks are expected to earn a higher return for investors than growth stocks; this result is intuitive. The first principle of investing is to “buy low, sell high.” Paying less to own the assets of the company is one of the best ways to make sure you are “buying low.” In the actual data, this premium for value stocks has proven to be significant. Over the last 91 years, value companies have outperformed growth companies by over 3% annually in the US. In international and emerging markets, the value premium has been even larger, as shown below (the shorter time frames for these markets are due to data availability): [2]

Because of this long-term benefit, we have structured our portfolios at PFG Investments to take advantage of this value premium. Our portfolios contain broadly diversified investments of thousands of companies across the entire market, tilted more towards value stocks. This tilt allows us to maintain a broad level of diversification and at the same time capture higher expected returns from value stocks.

We have seen the value premium for decades, and our expectation is that this premium will continue. However, we know that there may be periods of time where this premium does not appear in the short-term. Next week Nate will be hosting a webinar to highlight recent, short-term returns and what they mean for investors going forward. Be sure to check in again next week!

[1] Data from Morningstar, Inc. Accessed on November 11, 2020

[2] Information provided by Dimensional Fund Advisors LP. Past performance is no guarantee of future results. Actual returns may be lower. In USD. Indices are not available for direct investment. Index returns are not representative of actual portfolios and do not reflect costs and fees associated with an actual investment. MSCI indices are gross div. For US stocks, indices are Fama/French US Value Research Index minus the Fama/French US Growth Research Index. For developed ex US stocks, indices are Fama/French International Value Index minus the Fama/French International Growth Index. For Emerging Markets stocks, indices are Fama/French Emerging Markets Value Index minus Fama/French Emerging Markets Growth Index.